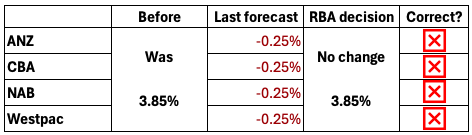

Last month the AFR reported that 32 of the 36 ‘experts’ it polled for their prediction of the RBA’s next interest rate movement were forecasting a reduction…but they were wrong! Here’s what the major banks were saying.

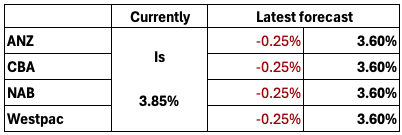

Here’s what they are saying now about what might happen on 12 August 2025.

What the ‘experts’ say about tomorrow’s change to target cash interest rate:

What the major banks say about the slightly longer term:

Source: bank websites

If NAB’s forecast was correct and the target cash rate was down to 2.85% by May 2026 and stayed at that level, the effective interest rate of over the next three years would be 3.15%. However, if ANZ is correct and there are only two cuts in 2025, this increases to 3.40%.

With banks adding about 2% margin to the cash rate, an equivalent 3-year fixed rate should be in the range of 5.15% to 5.4%. With some lenders announcing reductions in fixed interest rates last week, we see an increasing number of lenders offering 3 years rates in that range.

Interested in interest rates – UPDATE

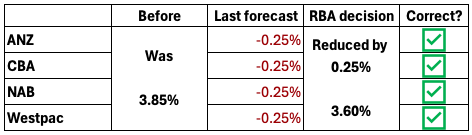

Published 12 August 2025

The RBA Board voted unanimously to lower the target cash interest rate by 0.25% to 3.6%.

How did the ‘experts’ do?

Whilst they all got it right this time, they do have different medium-term forecast. And we’ll be tracking these forecasts over the coming months.

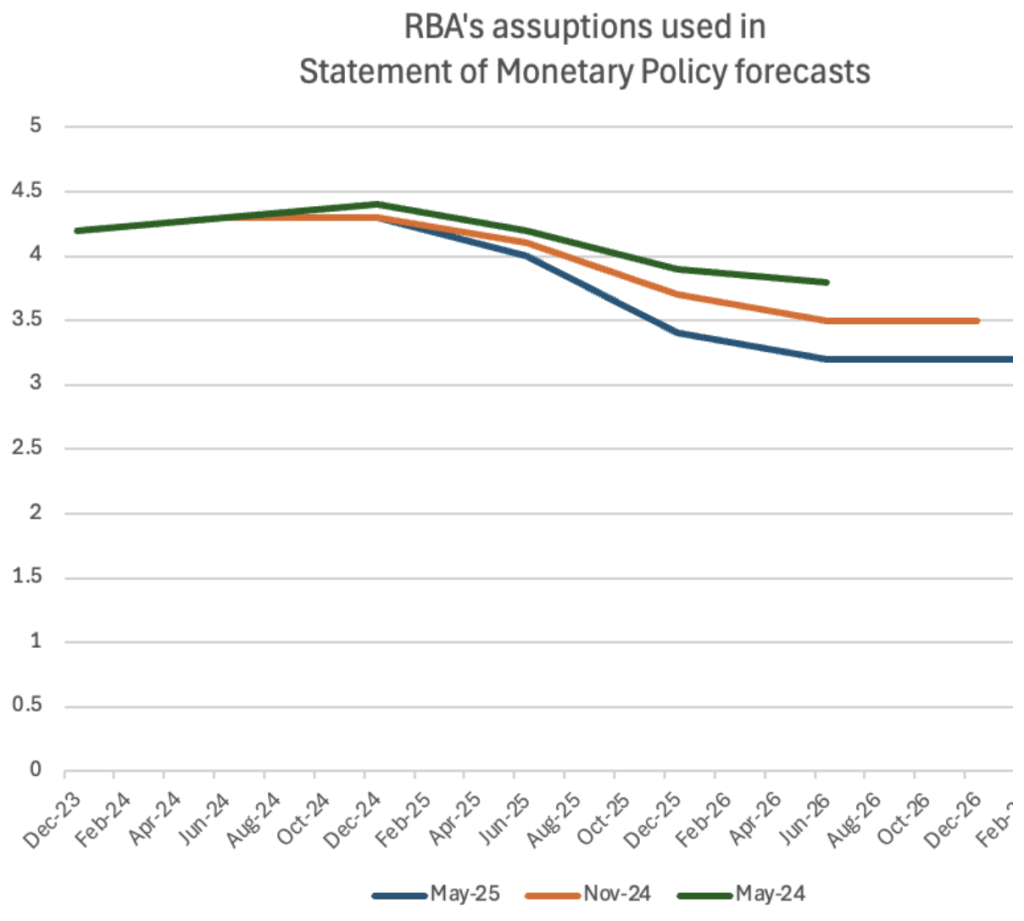

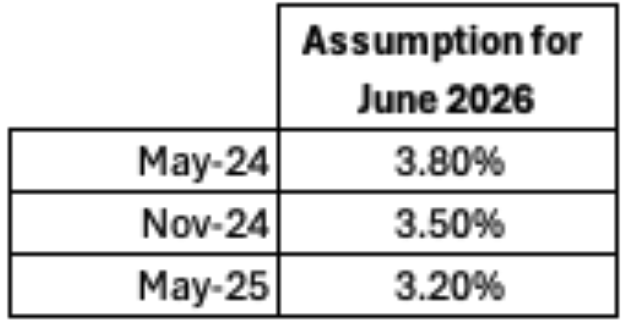

Forecasting interest rates is not easy! The Reserve Bank of Australia (RBA) assume an interest rate in their Statement of Monetary Policy (SMP). Here’s how they’ve done.

In the past two SMP, the RBA’s has lowered the cash rate assumption for the June 2026 forecasts

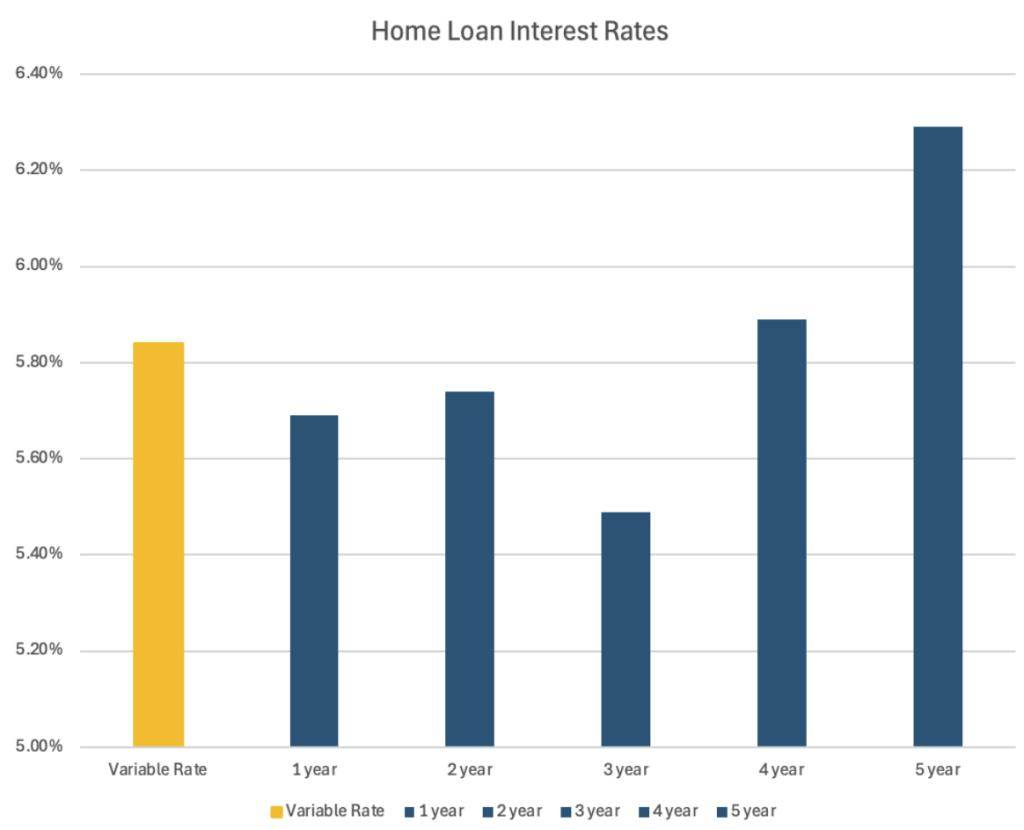

Here are some typical market home loan variable and fixed rates

We expect lenders to add a ~2% margin onto the cash rate. The most aggressive of the major bank forecasts is Westpac with the cash rate to drop to 2.85%. If they’re right, we would expect home loan variable interest rates to drop to ~4.85% Our estimate of the cost of a variable rate loan over the next 3 years, based on four 25bps drops in the cash rate, to be 5.15%.

Rates are indicative only, subject to change and lending assessment.Based on owner occupied, P&I loans with LVR less than 60% with a wealth packageComparison rates will be higher. Refer to your broker or EquateFinance.com.au for more information

*** Caution ***

There are many factors to consider when borrowing money including whether or not to fix the interest rate of some or all of the loan. Interest rates may affect your borrowing capacity as well as your repayment rates. Interest rates may impact lending products in many ways and lenders may apply interest rates differently depending on their circumstances & appetite and your credit strength & lending needs. We recommend consulting with a professional finance and mortgage broker.